* See Part 1 to learn about the Allens’ work for equality in the judicial system and World War II employment.

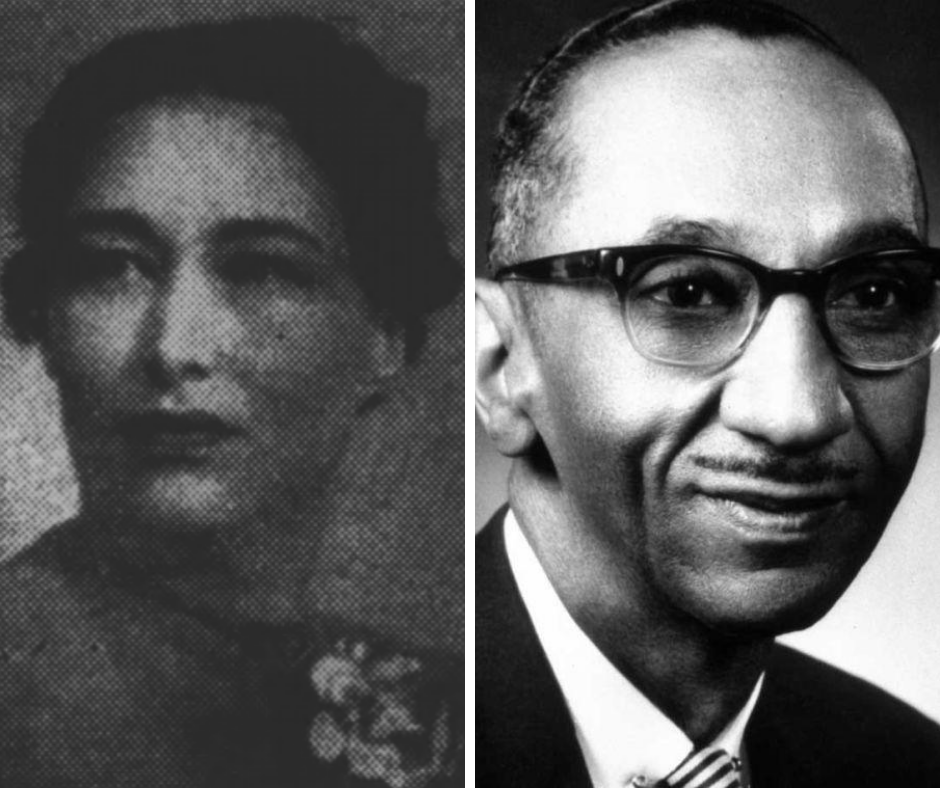

When the clouds of World War II lifted, South Bend activists and attorneys J. Chester and Elizabeth Allen had achieved many of their professional and philanthropic goals. The couple, who had opened their own law firm in 1939, had uplifted the Black community by crafting legislation, organizing social programs, and creating jobs. But institutional oppression and immense personal loss that followed in the war’s wake appeared to test their marriage. In these modern times of social unrest and pandemic-related stress, we can draw strength from the Allens’ ability to not only weather personal tragedy and systemic discrimination, but serve their community.

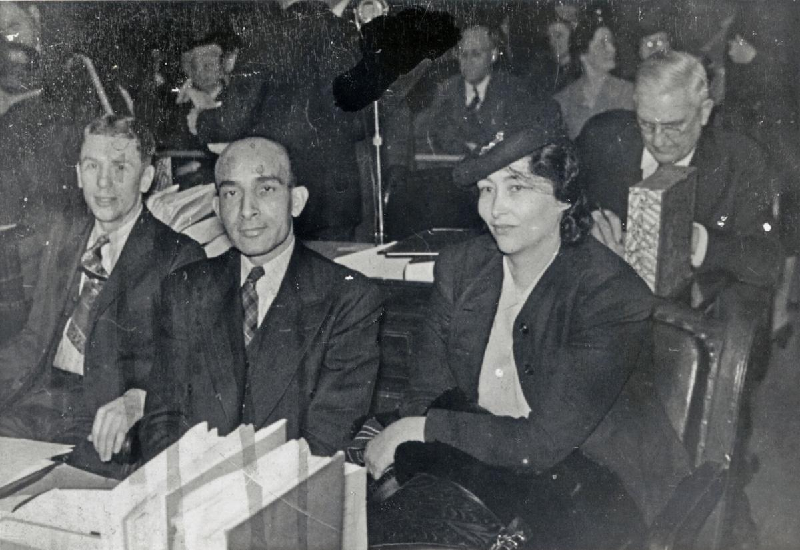

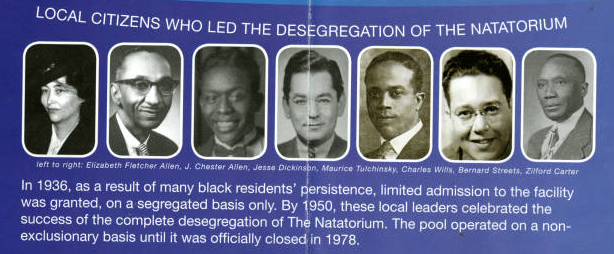

As the early Atomic Era unfurled, J. Chester plunged back into his fight to fully desegregate South Bend’s Engman Natatorium. The effort had begun in the 1930s and resulted in the park board’s meager concession of allowing Black residents to swim a few hours per week, when white residents were not there. In 1950, J. Chester and a group of attorneys, including white lawyer Maurice Tulchinsky, appeared before the parks board to again make the case for integration. Seemingly racism cloaked in Cold War rhetoric, one board member told the men that Tulchinsky’s involvement hinted at communist impulses. J. Chester replied, “‘You don’t have to be a communist to defend equal rights, opportunities and treatment for all people under the law. The Constitution and Bill of Rights mandate it.'” Threatening to file suit unless board members agreed to end segregation entirely, the lawyers at last won their long fight for equality, likely with the aid of Elizabeth Allen.

Oral history interviews and secondary sources suggest that Elizabeth drew up the original complaint and advised behind the scenes, pointing out that African American taxpayers helped fund the pool and therefore deserved to use it. Her name does not appear on official documents, perhaps because she was still in law school or because the lawyers feared that her involvement as a Black woman could hurt the cause. If Tulchinsky was accused of working on behalf of the Communist Party, one can only imagine what nefarious influences board members would assign Elizabeth if she was involved in the effort publicly.

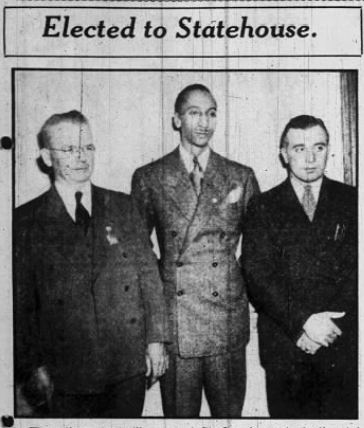

A series of interviews with the couple’s son, Dr. Irving Allen, bespeaks the constant frustration Elizabeth experienced from having to shelve her ambitions due to gender and familial norms and/or racial discrimination. In 1936, Elizabeth declared her candidacy for state representative, but withdrew, perhaps, because as interviewer David Healey suggested to Irving, she was “always overshadowed by circumstances” or “convinced that your father would have a better chance of winning.” Irving agreed that this sense of disappointment was probably compounded by the “loss and loneliness,” resulting from J. Chester’s absence while he served in the Indiana General Assembly between 1939 and 1941. Elizabeth could be “explosively judgmental” about J. Chester’s legislative efforts, accusing him of being too accommodating to white voters while campaigning. Perhaps this criticism stemmed partly from never having a chance to campaign for office herself.

Irving imagined the scrutiny she experienced as a Black female lawyer in South Bend during the “Dark Ages” of the 1930s, 1940s, and 1950s. He remembered his mother coming home and criticizing local judges “who she just despised and felt mistreated by.” This likely included Circuit Judge Dan Pyle, who in May 1952 fined her for contempt of court during a hearing in which she served as counsel. The South Bend Tribune reported that the “woman attorney” was fined for refusing to “abide by his instruction to refrain from dictating a lengthy statement for the court record.” Pyle ruled her “out of order in the request and demanded that she be quiet.” Irving recalled the incident, saying “she took it racially and cursed him out basically . . . and ended up in jail. Daddy got her out and got the whole thing, I think, squashed.”

Institutionalized discrimination and the stressors of working in the public eye seemed to breed resentment that spilled over into their marriage. The Allen household, while loving, was also highly-charged, in part because Elizabeth and J. Chester diverged sharply when it came to political allegiance and temperament. Irving recalled, “you were never sure whether the issues were where the vitriol was coming from or whether it was personal stuff that was being argued out through the politics.” But from a young age, Irving learned to tune out his parents’ disagreements. He stated there was “often too much venom involved in the . . . arguments about politics or nuances of how black folks could best be served in South Bend or the country.”

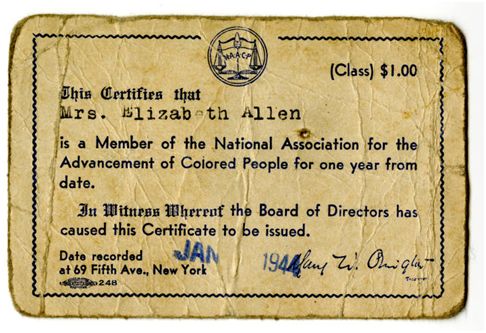

In Irving’s opinion, his parents were incapable of relaxing and resetting, prioritizing the needs of others over themselves in their work with organizations like the NAACP and Hering House. He noted that money was another source of tension for the Allens. Although they were attorneys, systemic racism affected their success and often meant they didn’t get the “big” cases. Determined that their children would get a good education, efforts to save for college proved stressful due to the lack of lucrative cases.

Irving suspected that the “pressures of work had enormous bearing” on his mother’s “existence.” Of his parents, Elizabeth had a poorer “capacity to separate work from the rest of her life. . . . I would just imagine the shit she took. Must have been unimaginable . . . unimaginable. And where’s it gonna go? It’s probably gonna come home into the relationship with her husband.” It surely did not go unnoticed that newspaper articles referred to her husband as “Attorney J. Chester Allen” and her as “Mrs. J. Chester Allen,” despite being an accomplished attorney in her own right. Probably equally frustrating, Elizabeth was subjected to scrutiny about her appearance and mannerisms in a way her husband undoubtedly was not, exemplified by this 1950 South Bend Tribune description: “feminine, but brusque. She has a no-nonsense attitude that contradicts the ultra-feminine hat on her head.”

Despite the many obstacles Elizabeth had to overcome, she received public recognition in 1953, 1955, and 1960, when she served as Judge Protem, filling in on occasion when the city judge was absent. “Her Madame Honor” was likely the first woman to wield a gavel in South Bend’s courtrooms. While a temporary role, Irving believed that the appointment was symbolic, honoring her legal career. Elizabeth worked to carve out educational and career opportunities for other Black women, generally relegated to domestic service in that era. Recognizing that de facto segregation would endure despite the landmark 1954 Brown v. Board of Education case, Elizabeth sprung into action, hosting an emergency meeting for the United Negro College Fund. She also worked to get Black women into her Alma Mater, Talladega College.

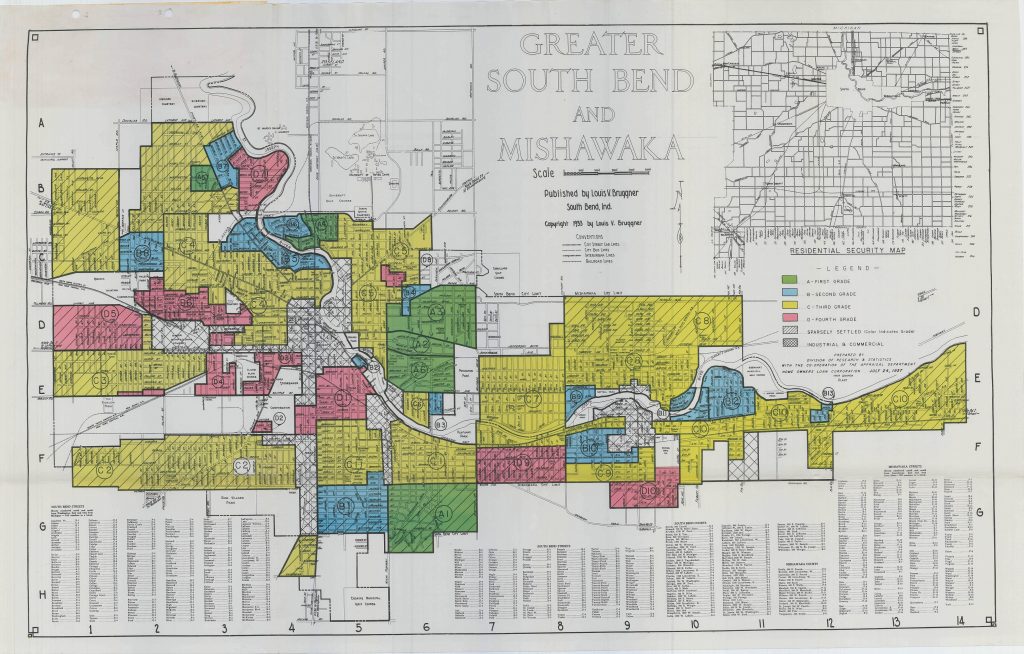

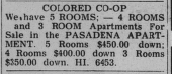

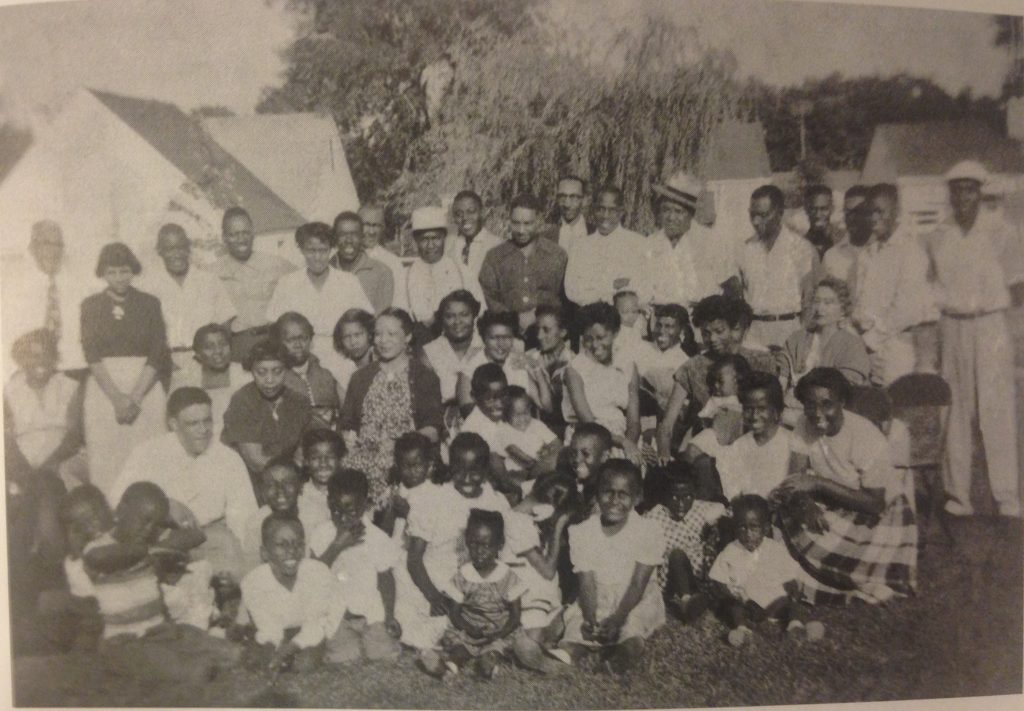

The Allens opened their house to Black Notre Dame students who had nowhere to stay due to discrimination and the housing shortage exasperated by World War II. Historian Emma Lou Thornbrough noted that in the 1940s many black families were forced to crowd into one or two bedroom units in substandard buildings. Elizabeth had worked during WWII and post-war years to improve housing options and clear local slums because “delinquency and crime are resulting from sub-standard housing.” In the 1950s, J. Chester helped a group of Black Studebaker workers navigate discriminatory lending and real estate practices to form a building cooperative called “Better Homes of South Bend.”

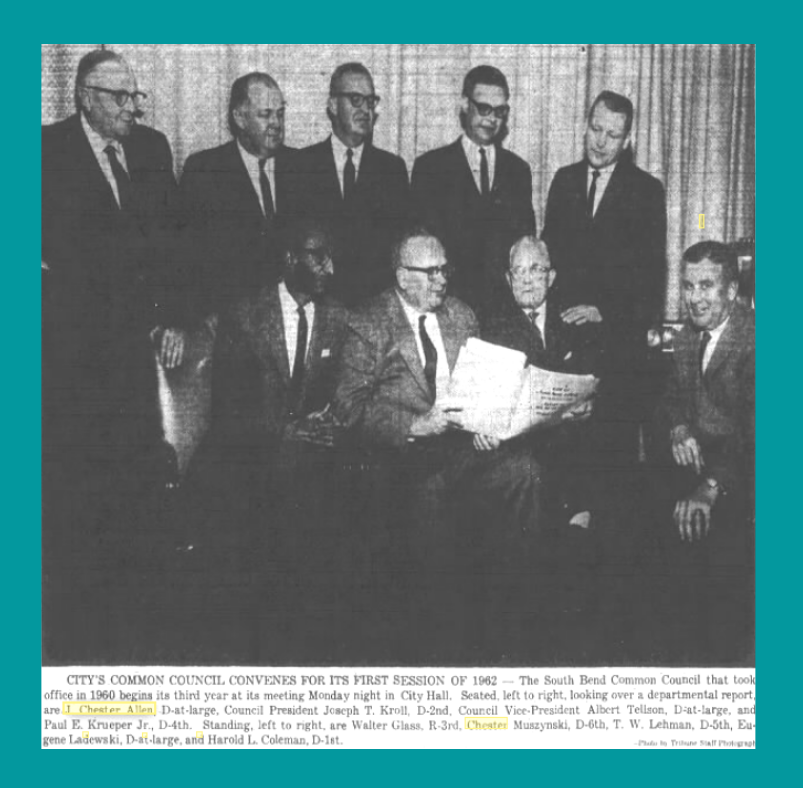

By the middle of the decade, twenty-two families of the co-op had moved in along North Elmer Street and helped build a vibrant community, filled with activities like family cookouts, kickball, and building snowmen. Irving described a “haunting aspect of the Better Homes story.” Although they had “outstanding credentials as good citizens and an established law practice,” the Allens encountered difficulties purchasing a home of their own. Perhaps such discrimination led J. Chester to further leverage housing reform when he was elected the city’s first Black Councilman in 1959. He quickly got to work trying to prevent the displacement of Black families as new developments arose. As Councilman he also got more African American appointed in city government. One Indianapolis Recorder writer was optimistic that Allen’s “devotion to the law as the shield of liberty” would enable him to “protect the rights of minorities and at the same time guard the welfare of the majority.”

J. Chester’s and Elizabeth’s work served as a tide that lifted many boats in St. Joseph County. But the couple soon experienced a devastating personal blow. Their daughter, Sarah-whom Irving described as a “brilliant student” at Central High School-was awarded honors at Wellesley College, before attending Tennessee’s Fisk University. In 1960, the South Bend Tribune noted an “illness forced her to leave college.” She had since been working as a secretary at the family’s law practice and receiving psychiatric care in her hometown. Shortly before dinner at the Allens’ house one summer evening in 1963, the family discovered that she had died by suicide. Only 27-years-old, Sarah undoubtedly possessed the astuteness and determination of her parents, but suffered from the era’s limited treatment options for mental health issues. Days after her passing, loves ones paid their respects at the city’s Episcopal Cathedral of St. James and the city council passed a resolution expressing sympathy for the loss of Councilman Allen’s daughter.

One can only imagine the impact such a catastrophic event had on the family. Perhaps it contributed to the fragmentation of the Allen and Allen law firm, which Irving said “kind of came unglued” in the early part of the decade. It’s possible it was the trigger for Elizabeth’s own hospitalization in the 1960s. Surely it contributed to the 1965 South Bend Tribune announcement of the couple’s separation after 37 years of marriage. Ultimately, the Allens chose not to go through with the divorce, perhaps a testament to their tenacity and love.

Work and community uplift likely became a haven from grief for the African American couple. In the years after her daughter’s passing, Elizabeth seemed to focus on advocating for women. She served as legislative chairman of the 1964 National Association of Negro Business and Professional Women’s Clubs, leading a workshop on “The Role of Business and Professional Women in the War on Poverty” at the organization’s annual meeting. Towards the end of the 1960s and into the 1970s, Elizabeth served on the board of St. Joseph’s first Planned Parenthood clinic. According to Irving, his mother was a feminist before the term existed. She would “go to war over women divorcing or getting beaten up by their husbands,” but, being ahead of her time, she fought a war “without any constituents.” Nevertheless, she was “‘incredible example to women—black or white.'”

J. Chester poured himself into education equality as the first Black member of the South Bend school board of trustees in 1966. One editorial contended that he was an ideal representative of Black educational interests, citing his “Quick intelligence, independence of thought, hard work and a genuine affection for his home community.” He used his legal skills in 1967 to advocate for equality, appealing a verdict that ruled the Linden School building, a Black school, could safely reopen despite a classroom ceiling collapsing during the school day.

While continuing to grieve, sons Irving and J. Chester Allen, Jr. pursued their professional goals. Their parents were determined that they would attend East Coast schools because, Irving noted, Black Americans had to be “twice as good” as their white colleagues. He earned his medical degree at Boston University in 1965 and practiced psychiatry in Massachusetts. Like his parents, J. Chester Jr. beat the drum for equality, leading an NAACP march protesting the police force’s refusal to hire a Black officer. He told the South Bend Tribune, “‘Maybe we’ll fill up that jail of theirs until they get tired of seeing us in it and hire one of us to get rid of the rest of us.'”

Like his parents, J. Chester Jr. was able to break racial barriers; he was sworn in as St. Joseph County’s first Black Superior Court Judge in 1976. Three years after J. Chester Jr.’s historic achievement, his father passed away. The man who had apparently stumbled upon South Bend did much to even its playing field for minorities. Black residents were better educated, politically- and civically-empowered, financially stabler, and able to enjoy the city’s facilities because of his tireless efforts as an attorney and elected official.

Unfortunately, his son’s promising career was cut short in 1983. J. Chester Jr. died of natural causes on Christmas Day, the same day his father was born in Pawtucket, Rhode Island in 1900. Matriarch Elizabeth Allen was now a widower who had lost two children. But her life was never defined by tragedy. In disregarding an admissions officer’s advice to forgo law school in favor of marriage years before, she started down a path canopied by improbable accomplishments, bitter disappointments, professional accolades, and personal heartbreak. Her fortitude and persistence meant that future generations would endure fewer obstacles than she did.

Behind her walked another Black female attorney from Chicago married to an ambitious Black attorney: First Lady Michelle Obama. The two women experienced the highs of professional accomplishments as a minority, the frustrations of sacrificing for their husband’s ambitions, public critiques of their appearance, and allegations of being too outspoken. Unlike Michelle, Elizabeth’s story has largely yet to be told, but South Bend writer Dr. Gabrielle Robinson and IHB are changing that by installing a state historical marker in 2021. Elizabeth, largely overshadowed by her husband, will quite literally have an equal share of recognition with this marker.

Sources:

“Public Angered at Whitewash,’” Indianapolis Recorder, June 1, 1935, 1, accessed Hoosier State Chronicles.

“Jellison Takes Petition to Run for Congress,” South Bend Tribune, February 16, 1936, 23, accessed Newspapers.com.

Mary Butler, “Mrs. Elizabeth Allen Lays Down Law to Family,” South Bend Tribune, July 30, 1950, 39, accessed Newspapers.com.

“Circuit Judge Fines Lawyer for Contempt,” South Bend Tribune, May 10, 1952, 8, accessed Newspapers.com.

“First Woman Presides City Judge,” South Bend Tribune, November 19, 1953, 29, accessed Newspapers.com.

“Field Chief Will Meet Fund Group,” South Bend Tribune, March 25, 1957, 24, accessed Newspapers.com.

Program, “Leaders for Workshops on Three Areas Affecting the Urban Family,” Woman’s Council for Human Relations, [1968], accessed Michiana Memory.

“Hon. J. Chester Allen,” Indianapolis Recorder, January 2, 1960, 1, accessed Hoosier State Chronicles.

“Adult Award Winner,” South Bend Urban League and Hering House, Annual Report, 1960, p. 5, accessed Michiana Memory.

“Sarah Allen Found Dead,” South Bend Tribune, July 25, 1963, 43, accessed Newspapers.com.

Nancy Kavadas, “Niles Area NACP [sic] Groups Conduct Orderly Demonstration,” South Bend Tribune, February 9, 1964, 8, accessed Newspapers.com.

“Divorce Cases Filed,” South Bend Tribune, March 5, 1965, 30, accessed Newspapers.com.

“Irving Allen Wins Degree,” South Bend Tribune, June 10, 1965, 46, accessed Newspapers.com.

Ruth Copeland et al., Plaintiffs-Appellants, v. South Bend Community School Corporation et al., Defendants-Appellees, 1967, 376 F.2d 585 (7th Cir. 1967), May 8, 1967, accessed JUSTIA US Law.

“Family Plan Unit Names Officers,” South Bend Tribune, January 26, 1968, 31, accessed Newspapers.com.

“Rites for Allen Wednesday,” South Bend Tribune, May 12, 1980, 21, accessed Newspapers.com.

“Wednesday Rites for Judge Allen,” South Bend Tribune, December 27, 1983, 28, accessed Newspapers.com.

“Allen, Former Civic Leader and Attorney, Dies at 89,” South Bend Tribune, December 28, 1994, 15, accessed Newspapers.com.

Marilyn Klimek, “Couple Led in Area Racial Integration,” South Bend Tribune, November 30, 1997, 15, accessed Newspapers.com.

Oral History Interview with Dr. Irving Allen, conducted by Dr. Les Lamon, IU South Bend Professor Emeritus, David Healey, and John Charles Bryant, Part 1 and Part 2, August 11, 2004, Civil Rights Heritage Center, courtesy of St. Joseph County Public Library, accessed Michiana Memory Digital Collection.

Barack Obama, A Promised Land (New York: Crown Publishing, 2020).

Email, Dr. Irving Allen to Nicole Poletika, March 19, 2021.